Kink & Taxes…

This article caught my attention not because of the headline, but because of what it signals underneath from a policy and tax-structure standpoint.

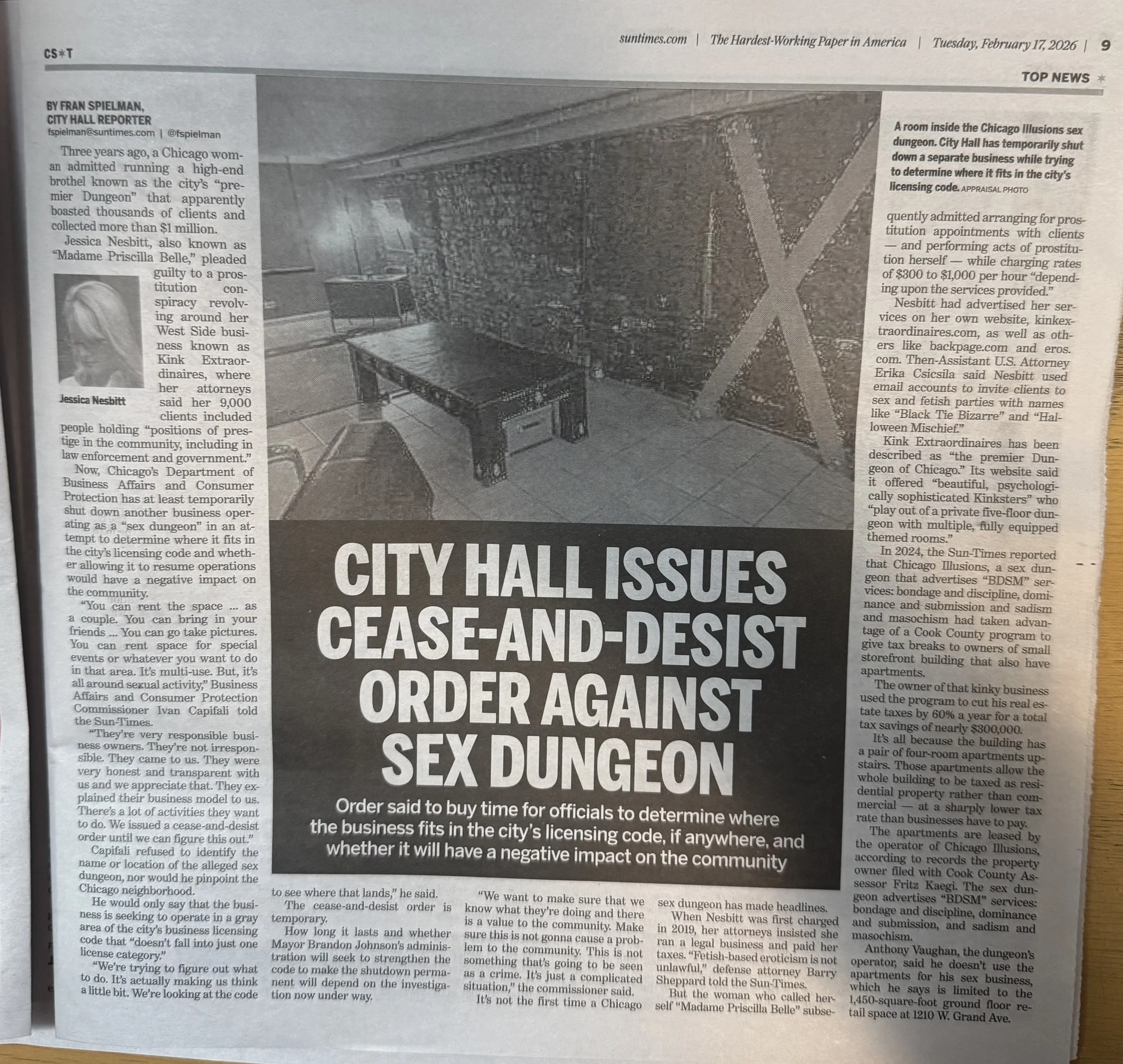

Strip away the sensational framing and what you’re really seeing is a city confronting a familiar problem: a use that doesn’t fit neatly into existing categories inside a mixed-use building. When officials say they are issuing a cease-and-desist “to determine where the business fits in the licensing code,” that is often the first step in something much larger than enforcement.

It’s the beginning of classification.

And classification is what drives taxation.

Cities rely heavily on clearly defined buckets, residential, commercial, light industrial, entertainment, etc. because each one carries different:

• property tax assessments

• licensing requirements

• occupancy rules

• insurance standards

• and revenue assumptions built into municipal budgets.

Mixed-use buildings have always lived in tension between those definitions. As new kinds of businesses, services, and experiences emerge, they blur the lines the tax code was written around decades ago. When that happens, municipalities don’t just regulate, they study, redefine, and eventually codify.

Historically, moments like this become the fact patterns used to justify ordinance changes:

“We encountered a use not contemplated by current code.”

“We needed tools to evaluate community impact.”

“We lacked a taxation or licensing mechanism.”

From there comes new language.

Then new categories.

Then new fee structures.

Then new taxable classifications applied not just to one operator, but to an entire class of properties.

That’s why these cases matter beyond the individual business involved. They can influence how cities treat mixed residential–commercial buildings broadly, especially older structures now being repurposed in ways zoning codes never anticipated.

The long-term question isn’t whether one operation is allowed or disallowed.

The real question is:

Will this lead to redefining how municipalities categorize and tax hybrid spaces going forward?

Because once a city rewrites definitions to “clarify,” that clarification rarely stays narrow. It becomes precedent. And precedent, in municipal governance, often shapes valuation models, compliance costs, and ultimately what property owners across the city pay.

This is how tax structures evolve, not through sweeping announcements, but through edge cases that force governments to redraw the lines.